While much of the focus of green (or ethical, or sustainable, or impact or responsible) finance has been on investing, the world of insurance offers many opportunities to green your financial safety net.

It’s clear that insurance companies could be doing far more than they are right now to clean up their own business behaviors … and be part of insuring against the consequences of climate heating rather than solely contributing to it.

But what about the reality of finding an insurer that really is green?

When we must buy insurance, how do you and I find a company that will help us and the planet?

In February 2026, I set out to find a real-green insurance company, but the search took far longer and was way more complicated that I was expecting.

The resulting blog was very long so I have broken the search into parts, for easier digestion.

- In this part, I cover defining green. I also check out four random B Corp insurance companies and four random insurance companies rated as green by green consumer magazines.

- In the second part, I dig into price comparison sites and check out four underwriters

- In the last part, I discuss whether you can be over-insured and conclude what I (and hopefully you) have learnt on this journey.

The Search Begins… Step 1

The first step is to define criteria for ‘green’.

The Greenhouse Gas Protocol (GHG Protocol) [1] was created in 1998, to help businesses and organisations identify, account for, and report on, gas emissions that contribute to climate warming.

In other words, report on their carbon footprint.

The GHG Protocol [1] reports on many climate heating gases like

- carbon dioxide (CO2)

- methane (CH4)

- nitrous oxide (N2O)

- hydrofluorocarbons (HFCs)

- perfluorocarbons (PFCs)

- sulphur hexafluoride (SF6)

- nitrogen trifluoride (NF3).

Other climate heating gases (e.g. CFCs, NOx) are reported separately.

The idea behind the GHG Protocol was to develop an internationally accepted accounting protocol that would encourage businesses to be transparent about their emissions. It aimed to help business create a standard baseline against which to compare the results of ongoing actions that could reduce climate-heating gas emissions.

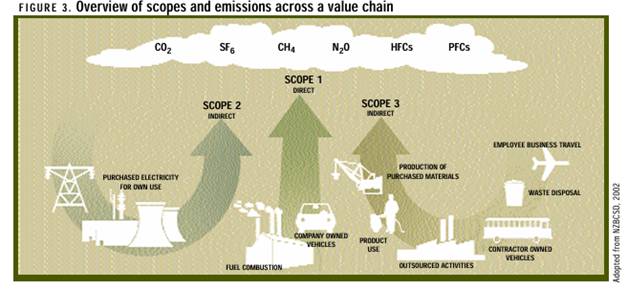

The GHG protocol classifies operational control of an organisation’s activities as either Scope 1, 2 or 3. It delves deeply into how to quantify emissions, but for purpose of this post, I want to pay attention to the GHG attempt to unravel responsibility and control through classification of SCOPEs (see figure below [1, p26]):

The three scopes are:

- Operations that a company controls or fully own.

For example: for an insurance broker, Scope 1 emissions would include gases emitted by their office buildings, digital purchases, internet use etc. Since these emissions are under direct control of a business, these are ultimately the most reduce-able.

- Company energy use.

This means energy used by the company to power their Scope 1 activities. When a power company burns fuel (e.g., gas, coal) or uses renewables to generate electricity, the resulting emissions occur at the power plant but the company that buys and uses that electricity is responsible for those emissions under Scope 2. So back to our insurance broker, Scope 2 emissions would be the emissions from electricity purchased by them.

- Supply chain of a company, both upstream and downstream.

For any business or organisation, most emissions will ultimately lie in their supply chains and are much more difficult to control. Reducing Scope 3 emissions takes time and significant engagement between a company and its myriad suppliers. For example, an insurance broker’s scope 3 emissions would lie with the underwriting insurance company, how the underwriter invests the ‘float’, their use of data centers, telematics and artificial intelligence, how claims money is spent (such as car repairs, or renovations after a flood, medical care in a travel emergency…) and so on. As you can see, Scope 3 gets complicated very quickly.

And as you might expect, there are numerous criticisms about the GHG Protocol, that its loopholes and inaccuracies allow greenwashing and the often-used approach of ‘counting’ emissions then claiming ‘net zero’ through carbon offsets without tangible business behaviour change. Not least, the GHG Protocol creates a metric for financialization of something that is freely available, is everywhere, and is essential to life.

On the other practical hand, the GHG Protocol is a widely used standard in the current times and can be used to measure change, however imperfect.

We can work with imperfection and use GHG accounting as a criterion to assess insurance companies on their ‘green-ness’ by asking a simple question:

Are insurance companies…

- REPORTING their GHG emissions

- doing so CONSISTENTLY

- and REDUCING their emissions over time.

Let’s find out.

Step 2

I started by looking for companies that were already reporting their carbon emissions.

The ‘Certified B Corporation’ badge is awarded by a non-profit organisation called B Lab. The badge acts as a claim that the company has self-assessed itself as achieving a “high” (according to B Lab) standard of social and environmental performance, transparency and accountability [2].

I searched the B Lab directory for insurance companies in February 2026. The search terms used were: UK HQ; financial services/non-life /other insurance and selected a random four companies from the results.

These four are summarised in the table below.

ESG is short for environmental, social, and governance factors addressed by a company. I used it in the search to find GHG reports.

| Name | Type | ESG Reporting? | Content? |

| Fuzzy Insurance | Broker. Underwriters: Unspecified | No | None |

| Yulife Holdings | Broker. Underwriters: AIG Life, Bupa, MetLife UK Ltd, Zurich | Yes | Charity donations |

| Urban Jungle Service Ltd | Broker. Underwriters: AXA, Allianz, Ageas UK Tradex, AmTrust Specialty Ltd | Yes | Carbon Offsets. Statements on reducing emissions but no evidence. |

| Bikmo | Broker. Underwriter: Hiscox Underwriting Ltd/ Uniqua | Yes | Detailed carbon footprint. |

Step 3

Now we figure out what we’ve got.

- Fuzzy had a relatively high B Corp score but no further discussion of sustainability on its website. I mention B Corp scores because I had initially assumed that a higher score meant a ‘greener’ company – but this was not borne out by the availability of GHG emissions reporting.

- Yulife see their ‘green’ activities as gift giving, which was not the criteria I used.

- Urban Jungle had a significantly higher B Corp score than the others (though scores published before 2026 were self-assessed) and discuss sustainability on their website – but don’t back up claims with evidence.

- Bikmo stands out by being explicit on their GHG emissions, their claims, actions taken, and actions not taken in five annual reports. Total carbon footprint is given in annual impact reports with percentage allocation to Scope 1,2, 3 (method not stated) – total carbon has increased over period with company growth and learning how to count emissions.

Step 3

I loved Bikmo’s transparency. As well as reporting emissions, they stated what they had promised to do but didn’t actually get round to.

However, their insurance is limited to bikes. Unfortunately, then, Bikmo can’t help us with insurance for other things (like car, home, or life insurance).

I also realised that insurance is often sold through brokerages rather than direct from an underwriter, and that many brokerages are owned by a wider group. In the next step I dug deeper into the broker companies to find out more about their parent.

Step 4

During March 2026, I searched on my browser for “which insurance company is the greenest?” and selected those rated by consumer magazines as ethical.

I randomly chose four companies to quickly check their credentials.

The results are in the table below.

| Name | Business | GHG Reporting? | Any Impact Reporting? |

| Naturesave | Broker. Subsidiary of Lloyd & Whyte who are part of Benefact Group. Underwriter: Ecclesiastical and Ansvar. | No | Ethical statement. Charity donations. Plant-a-tree. |

| Environmental Transport Association (ETA) | Broker. Underwriters: ARAG Legal Expenses Insurance Company Ltd (car insurance). Red Sands Insurance Company (Europe) Ltd (cycles/Mobility Scooters/Powered Chairs) | No | Environmental campaigns. |

| Arma Karma | Broker. Underwriters: Bspoke Underwriting Ltd / Watford Insurance Company Europe Ltd (personal items insurance) | A total count by Ecologi | Charity donations. |

| Evergreen Insurance | Broker. Underwriters: Ageas, Allianz, Aviva, Axa, Liverpool Victoria, Markerstudy, QBE, Intact, Zurich (personal, business, travel insurances) | No | Ethical statement. Charity donations. |

Step 6

While digging deeper to find their emissions reports and more about the parent company itself, I found that:

- NatureSave is a brand name of Naturesave Policies Ltd that was acquired by Lloyd & Whyte Group Ltd in 2022 that itself was acquired by Benefact Broking & Advisory Holdings Ltd in 2023 (owned by Benefact Group PLC). Neither Naturesave nor Lloyd & Whtye reported on their GHG emissions. Benefact Group’s Annual Report did report on GHG emissions for years 2021, 2022, 2023 and 2024 using the Streamlined Energy and Carbon Reporting framework that is mandatory for public limited companies in the UK. Reported emissions doubled between 2021 and 2023 and fell 10% (compared to 2023) in 2024 [3].

- ETA is owned by Two Three Bird Holdings Ltd and ultimately controlled by the Grobler Investment Family Trust according to the Companies House Register. No GHG emissions reporting was found on the website of Two Three Bird Ltd. ETA state on their website that in 2002 they “became the world’s first carbon neutral motoring organization” (via carbon offsets with Gold Standard projects). However, I couldn’t find reports of their GHG emissions to back up this statement. The Grobler Investment Family Trust appears to be registered in South Africa and no GHG emissions reports were found by date of this post.

- The Arma Karma uses a company called Ecologi to count and offset their GHG emissions. The Ecologi website gives CO2 avoided in metric tonnes which implies that Arma Karma is counting its GHG emissions. However, I couldn’t find GHG emissions reports on the Arma Karma website to back up this statement. Arma Karma is a wholly owned subsidiary of BSpoke Insurance Group Ltd, which reports charity donations made and volunteering enabled. BSpoke itself is controlled by NFP UK Holdings Ltd who were on the FCA register as an Appointed Representative of Innovative Risk Labs Ltd. Innovative Risk Labs Ltd is a London-based insurtech broker and incubator. At date of this blog post, none of these entities were reporting GHG emissions.

- Evergreen Insurance is a trading name of Surrey Independent Advisers Ltd (an insurance brokerage). According to Companies House register, the brokerage is 75% or more owned by J.M. Glendinning Group Limited. Evergreen has a webpage clearly stating which companies are underwriting the policies they sell and were the easiest of the four to find the underwriters. Neither Evergreen nor Surrey Independent Advisers report their GHG emissions. No website for J M Glendining Group Ltd was found at date of this blog post.

This step took far longer than I was expecting.

The insurance companies, again, turned out to be brokers so I spent a lot of time trying to figure out who actually owned the supposedly-green insurance company and whether the ultimate parent company was actually reporting their GHG emissions instead of something else, such as making statements on charity work for instance.

Step 7

Decision time.

A check-up on 4 insurance companies recommended by ‘green consumer’ websites found 4 brokers of which only one parent company was providing their GHG emissions reports using the SECR method. The SECR method mandates Scope 1 and 2 reported in full and voluntary reporting on Scope 3 [4] – Benefact Group reported employee mileage only for Scope 3.

So I’ve found at least one parent company that is reporting its GHG emissions consistently and showing reduction. One is better than none but at least two would be better, so let’s keep looking in the second part, here (LINK TO FOLLOW).

References

[1] World Resources Institute (2004/2015) The GHG Protocol Corporate Accounting and Reporting Standard Revised Edition https://www.wri.org/initiatives/greenhouse-gas-protocol

[2] B Corp https://bcorporation.uk/about-b-lab-uk/b-lab-uk/our-standards/

[3] Benefact Group (2024) Annual Report and Accounts 2024: Together Building a Movement for Good Gloucester. [4] Seedling (2026) SECR Reporting Requirements & Guidance: How to Complyhttps://www.seedling.earth/post/our-secr-reporting-guidance