Insurance is often called protection because it claims to protect you from financial loss in adverse future circumstances.

It’s an unfortunate term for anyone coming from global health because protection is associated with pregnancy avoidance and has a sense of preventing an unwanted condition. However, insurance doesn’t prevent a disaster taking place, it’s more like post-disaster-consequences-containment.

There’s plenty chatter on the internet about green insurance products or premium discounts for ‘sustainable’ behaviour. For instance, insurance for electric vehicles and renewables, or premium discounts for using recycled materials in home newbuilds or repairs [1].

But is that it? Is that all it takes for insurance to be ‘green’?

Let’s go back to the start with a definition.

What is Insurance?

First of all, insurance is an industry.

In 2023, Berkshire Hathaway from the USA was the largest insurer worldwide by revenue, the next being Ping An Insurance, China [2].

In 2025, the UK insurance industry managed £1.91 trillion in investments [3], of which £31.4 billion was for motor insurance. EV insurance premiums are around 18.5% lower than conventional vehicles. Insurers are increasingly using telematics, AI-powered digital identity tools and predictive analysis along with blockchain adoption for data security and transparency [3].

Telematics, AI, EVs, blockchain, predictive analytics… these all come with high energy consumption and dependence on rare earth minerals that have shown to be ecologically unfriendly. Add in the multiplier effect of claims and “the indirect impact of insurance can extend to some 10% of the world’s GDP” [8]. Insurance is, then, a lucrative, global industry.

Second, insurance is a float.

Warren Buffet calls insurance a float – money that doesn’t belong to him but that he has the use of [4].

When an insurance company receives premiums, it may not need to pay out claims at all or there may be a significant time gap until claims are made (e.g. in life insurance). The time gap means that the premiums can act like a float – a cash reserve that allows an insurance company to invest in bonds, stocks, company takeovers… These investments can themselves go on to generate cash flow that enable an ambitious company like Berkshire Hathaway to buy more insurance companies that generate more premiums to invest … and so on.

To make this work, Berkshire Hathaway controls how insurance is underwritten by the group’s insurance companies. When premium prices are low, fewer policies are written. When pricing are high, more policies can be written [5].

But such a strategy depends on an insurance company being careful about who it is willing to insure in the first place. To be profitable, underwriting needs to ensure that total costs of providing insurance and meeting claims are lower than the value of premiums coming. The company also needs to be able to raise premiums when needed to ensure that the company costs/premium price ratio stays low and claims are minimized.

At the same time, insurance companies fear insolvency. The Prudential Regulation Authority in London, for instance, applies strict solvency requirements on insurance companies to prevent systemic financial collapse.

From the point of view of the insurance company, this strategy can ensure solvency and a float to invest. But from the point of view of a single policy holder, it can result in higher premiums or refusal to cover risks that are highly likely to materialize.

This takes us to a third definition.

Insurance is most often defined as risk transfer.

Risk Transfer and Underwriting

Imagine two hill walkers climbing the UK’s highest mountain on a sunny day. One is in plimsoles, T-shirt and shorts and has packed lunch and water in his bag; the other is in boots, joggers and T shirt, has packed lunch, water, energy snacks, rain jacket, hat and gloves, and told the hotel reception her route and expected return time. Which climber would you bet makes it to the top and back down again in one healthy piece?

Anyone that ever went up a hill would pick the second. Because you don’t take the cold weather gear up a mountain to use it, you take it because you might possibly need it.

This possible future need is called risk. The most idealistic definition of any kind of insurance is that it’s a transfer of risk of financial loss.

So how does that risk transfer work.

Let’s consider natural disasters.

High winds, earthquake, tornado-hail, wildfire, and inland flooding are all natural disasters that become increasingly likely as our world heats up. Catastrophe models (cat models) are used to quantify risk, using mathematical simulations to assess the potential impact of natural or man-made disasters. These models incorporate numerous data points such as geography, building structures, past disaster occurrences, historic loss data, magnitude and ground shaking for historic earthquakes, central pressure and wind speeds for historic hurricanes and so on. The model can then estimate potential loss and damage from future possible events [6]. Pure premiums are estimated in two ways: Probable Maximum Loss, the worst-case loss expected within a given return period (e.g., 1-in-250 years). And Average Annual Loss, which estimates the expected yearly loss under stable climate conditions [6].

Cat models help insurers assess risk, set premiums, determine reinsurance needs and comply with solvency regulations. They are used not only by insurance companies but also rating agencies, retailers, wholesale brokers, reinsurance companies, risk managers and state regulatory boards [6]. There is debate about the extent to which climate models can or should be integrated into catastrophe models given the uncertainty about causal relations between climate change and a catastrophic event [7].

Even the best run insurance company will hit a limit in its willingness to accept other people’s risks.

This is called the ‘retention limit’ . When an insurance company hits their retention limit, it will seek reinsurance. Reinsurance is insurance-for-insurance-companies and allows an insurer to transfer part of their risk to another insurer (the reinsurer) in exchange for a premium. That is to say, for large risks such as natural disaster insurance, both the policy holder and the insurance company are paying premiums. Reinsurance helps insurers manage large and potentially catastrophic losses, ultimately to ensure solvency.

As a rule of thumb in underwriting, the greater the likelihood of a risk materilising, the more expensive the premium. In a context when climate related disasters become increasingly likely, the logical next step is that premiums go up or coverage is discontinued.

In the wake of escalating wildfires in California, many insurance companies paused or withdrew buildings coverage in parts of the state. Financial risks to insurance companies providing fire protection grow as wildfires become more frequent and severe. The costs of reinsurance also rise. In response, the California Department of Insurance has implemented ‘California’s Sustainable Insurance Strategy’. A key point is that previous insurance regulations kept policy prices low by requiring insurers to use historical catastrophe data to price policies. But new regulations allow use of forward-looking climate models and future pricing. This aims to attract insurers back to covering wildfires along with incentives for homeowners to “fireproof” their homes. Even though these changes mean that individual policy costs will rise significantly [9], they do not guarantee that insurance companies will be willing to cover wildfires.

Green Insurance Products

So where do the insurance polices that you, and I, buy come in?

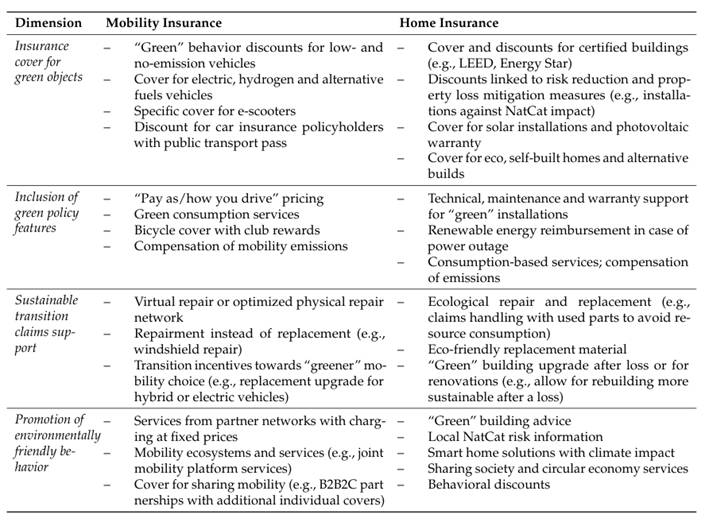

Various ‘green insurance products’ do exist but there is no consistent definition. The claim for a green insurance product tends to rest on it being insurance for an object or activity that is considered green in some way.

Some examples in home and mobility insurance are given below [excerpt from 8].

Insurance cover for ‘green’ objects can come with special pricing to attract purchase and use. Or insurance products can support sustainability themes, for instance, encourage circular economy by paying for repair instead of replacement and supporting innovations in green buildings. Such insurance products can help speed up transition to a cleaner economy and are highly relevant.

But claims of greenness need to backed up with transparent data on how, and by how much, such products generate their own greenhouse gas emissions and how far they reduce emissions in other areas by discouraging consumption.

A claim of greenness, without evidence, is merely greenwashing.

Some insurance companies that initially signed up to the United Nations Environment Programme voluntary Principles for Sustainable Insurance(UNEP PSI) in 2012 did indeed disclose emissions (for instance, SwissRe, part owned by Berkshire Hathaway).

The UNEP PSI proposed global frameworks for the insurance industry to address their ESG risks and take advantage of business opportunities opening up through the transition. A Net Zero Insurance Alliance was launched in 2021 to help underwriters and investment managers reduce greenhouse gas emissions through their underwriting/investment processes. But by 2023, many early members had left citing a letter from U.S. state attorneys general that collaboration on climate goals could violate American antitrust laws and state regulations. It later closed and was replaced with a less contentious ‘Forum for Insurance Transition to Net Zero’ [10].

Which is a pity. Because a 2025 survey indicates that individual insurers as well at the industry generally is unprepared for the changes in climate and the rising physical risks that we are experiencing [11].

And so…

Can insurance be green?

Insurance can encourage the economic transition to a greener economy.

Insurers could use high premium prices to discourage destructive behaviors. They could encourage climate risk management and encourage climate resilient behaviour in a ranges of sectors. They could find innovative ways to offer covers for increasingly common physical risks.

However, it also looks like insurance companies have been reluctant to fully embrace these possibilities and are amenable to political pressures.

The float is the largest unknown. How is the float being used by insurance companies – is it financing coal, gas and oil companies to drill, refine, sell, and burn hydrocarbons that are driving global heating, escalating natural disasters like wildfires, and making home insurance unobtainable?

And if we want to buy insurance from a green insurer, how do we find one?

A different post takes up this question.

References

[1] Insurance Information Institute (no date) Green Insurance https://www.iii.org/article/green-insurance

[2] Statista (2025) Leading Countries By Life Non-Life Premiums Written https://www.statista.com/statistics/217257/leading-countries-by-life-and-nonlife-premiums-written/

[3] Burnett, S (2025) UK Insurance Industry Statistics 2026: Trends, Data, and Market Analysis https://coinlaw.io/uk-insurance-industry-statistics/

[4] Mead, A (no date) Warren Buffett Explains How A $7 Billion Liability Is Better Than Equity (1996) https://www.youtube.com/watch?v=qDuWOkD0d5E.

[5] Dematos, D (2025) Berkshire Hathaway and Insurance (Part I: National Indemnity) https://tontinecoffeehouse.com/2025/02/03/berkshire-hathaway-and-insurance-part-1-national-indemnity/

[6] Amwins (2025) What’s New In Cat Modelling? https://www.amwins.com/resources-and-insights/market-insights/article/what-s-new-in-cat-modeling.

[7] Vaughn, S (2023) The Morality of Investment Stigma and Insurance in Climate Governance Public Culture https://doi.10.1215/08992363-10742565

[8] Stricker, L et al (2022) Green Insurance: A Roadmap for Executive Management Journal of Risk and Financial Management https://doi.org/10.3390/jrfm 15050221

[9] Paskerian, M (2025) Insurance Under Fire: Assessing How California’s Insurance Industry is Tackling the Wildfire Crisis and What’s Next University California Law Journal https://repository.uclawsf.edu/hastings_law_journal/vol76/iss6/11

[10] UNEP https://www.unepfi.org/insurance/

[11] Mahmood et al (2026) What the Market Thinks: How Global Insurers are Responding to Rising Physical Risk MSCI Institute