This post was revised and edited on 1st July 2025.

It has been said that there is little climate finance to support the transition to low-carbon nature positive and climate-resilient heath systems [1]. The health sector can fall through gaps in general climate financing, while climate falls through similar gaps in traditional healthcare financing.

This being the case, where then is the money for climate adaptation and mitigation in the health sector?

Three options were considered previously. They were:

- Grants;

- On-budget;

- User fees.

Here the focus is Debt.

In global health financing, there is very little conversation about national debt but its massively influential on health systems in low resource settings.

Globally, healthcare must change but how does debt-based climate finance impact on health financing and the ability of health sectors to fund their transition?

Debt and the Cost of Change

There are numerous debt-based instruments used in international development and any discussion can quickly get complicated and overly technical.

The key point I want to make here is that debt is perceived to be an essential element in the financing mix.

The word perceived is important. Because I think debt is not automatically essential to fund a green transition.

You may have seen statements like this:

- “annual climate finance flows must increase by at least sixfold compared to current levels,reaching US$8.5 trillion per year between now and 2030, and over US$10 trillion per year from 2031 to 2050” [2].

- annual climate finance could be “1.1% of GDP, on average, in upper-middle-income countries… 5.1% of GDP in lower-middle-income countries and as much as 8.0% in low-income countries” [3]

- “the world faces a $US41 trillion mitigation investment gap to 2030…and adaptation financing gap of $US600 billion required annually to 2050” [4].

These reports and articles then go onto to pose an implicit question:

where can such a VOLUME of finance be found?

Government (public sector) is considered to have insufficient revenue. And grants are notoriously few.

An inevitable conclusion is that debt is essential to fund the green transition.

An Independent High-Level Expert Group on Climate Finance states specifically that financing for carbon mitigation, climate adaptation, and nature positive land-use is “a trade-off between taking on more debt for the right kind of investments”. The same group acknowledges that current and significant debt distress in many countries and that any “debt and financing strategy (should) tackle(s) festering debt difficulties” enabling a major expansion [5] of finance. Presumably more debt…

Global statements like these can be vague. It’s not clear…

- who are the lenders?

- who would be taking out such debts?

- who would be paying the interest on these debts?

- who would receive the interest?

- when and who would eventually pay back the debt?

Low and middle income country governments (here LMICs) are taking on more and more debt.

The external debt stock of LMICs across all world regions was US$9.0 trillion in 2022 [6].

In full, that is US$9,000,000,000,000.

In East Asia & the Pacific, total external debt was US$3,345 billion in 2022 with a balance towards long term debt. Public and publicly guaranteed interest payments totaled US$66billion in the same year, “the highest level in history” and expected to keep growing. The Lao PDR and Mongolia are the most vulnerable, due to previously high levels of debt. Their debts are largely held at variable interest rates and denominated in foreign currency [6]. These last two factors mean it’s much harder for government to control the size of their debt and repayments.

Discussions on debt quickly get incomprehensible, so I want to keep two points in mind here:

- Debt is advocated by international finance organisations as essential for the green transition;

- Many LMICs are already highly indebted from historical borrowing and ongoing debt servicing.

Historical Debt and Health

The question of who takes on debt and who pays it back is critical. Because historically, social-safety nets like health and education have been part of paying back national debts.

The impact of national debt on health has been discussed elsewhere [e.g. 7]. In summary, the global financial crises of 2008, 2011 and more recently with COVID, all impacted heavily on LMICs, which had previously experienced high annual economic growth. When their economies shrank during and after such crises, government expenditures tended to stay high meaning that government revenue exceeded government income. To make good the shortfall, governments turned to their reserves.

After these reserves were exhausted, the next step was to borrow funds to pay for expenditure.

The external debt stock of LMICs grew from US$479 billion in 2012 to US$1.1 trillion by 2022 [6]. Within that period other shocks such as knock-on from the war in Ukraine and climate disasters further reduced the financial resilience of countries.

So where is the health sector in this?

Debt reduces government space to invest into health. LMIC governments spent about 2·21% GDP on health in 2020. In the same year, just over 1·97% GDP was spent on interest payments [6].

Interest payments and debt repayment divert public spending away from health as well as other critical social support sectors. Debt and a pressing need to pay interest on that debt, focuses attention on increasing economic growth. However, since the returns from economic growth are at least partially returned to the lender through interest payments and not fully invested nationally, debt-servicing costs can correlate with lower economic growth.

When government runs large annual budget deficits, it can spur inflation in emerging economies, especially those with high share of foreign currency debt [8]. For instance, in Lao PDR, with extremely high levels of debt, headline inflation rose significantly to 39.3% by the end of 2022. Inflation in medical care was around 27% [9]. Inflation means that costs are rising – cost of staff wages, medical supplies, transportation, energy and so on. Costs increase and compound across the health system not just at point of healthcare delivery. Increased costs can therefore prevent or reduce access to care, and influence management decisions. Decisions like… which services are financially viable now? Which hospitals/health centres should close to save money? What staffing levels can be maintained?

High levels of public debt can set up a cycle of reduced investment into healthcare, which leads to reduced preparedness for natural disasters. This generates higher fatalities from a specific disaster event, along with unrepaired loss and damage to health infrastructure and procurement systems.

The upshot is a situation where the health sector’s resilience for the next disaster is undermined [10] so that overall, the health sector weakens over time.

But disasters can also impair economic growth. COVID19 was a health pandemic and it shocked every national economy, radically reducing national income and ability to pay interest and make debt repayments.

It is widely acknowledged that climate chaos will create economic shocks and will reduce economic growth – but by how much and for how long is highly uncertain. At the same time, history shows that national debt has been destabilising for publicly provided healthcare.

Now, let’s imagine a scenario whereby one sector of the economy, for instance publicly owned energy generation and transmission, takes on external debt to pay for their green transition.

Public Sector Debt and Climate Finance

As an example, let’s focus on the finance of the JETP.

Just Energy Transition Partnerships (JETPs) are multilateral platforms between an international partner group, mainly France, Germany, United Kingdom, United States and the European Union, though additionally including Japan, Norway, France, Germany, Italy, and Denmark in the Southeast Asian JETPs and a LMIC country.

So far only 4 exist in the world: South Africa and Senegal, Indonesia and Vietnam. I focus here on the Southeast Asian JETPs.

JETP have been called an innovative financing response to accelerate the energy transition for an equitable and socially inclusive low-carbon energy grid. This discussion focuses only on the financing element of JETP.

The justification for a JETP is the extremely high costs of overhauling a carbon-based energy sector: “close to” US$50billon in Indonesia and Vietnam (each) [11] or specifically:

- “Indonesia requires a staggering US$66.9 billion to fund over 400 priority projects aimed at achieving its power sector transition pathway goals by 2030” [12].

- Vietnamese power sector “needs US$135 billion to (stop)…issuance of permits for new coal plants, build(…) new renewable power plants, and upgrade(…) its electricity grids” [12].

The question is posed – where can such volume of finance be found?

“JETPs are designed as catalytic mechanisms, aiming to improve conditions for private investment in renewable energy. For example, in the cases of Indonesia and Vietnam, the pledges of concessional capital from the International Partners Group were matched by private sector investment pledges for the first time, coordinated by the Glasgow Financial Alliance for Net Zero” [11 emphasis added].

The JETP financing mechanism is massive in scale [12], even compared to other more mature multilateral funds for climate change, such as the Green Climate Fund (GCF), the Global Environment Facility (GEF) or Reducing Emissions from Deforestation and Forest Degradation in Developing countries (REDD+). For instance:

- GCF has disbursed US$13.5 billion (excluding co-financing) since 2015.

- GEF has disbursed US$30 billion since the 1990s.

- REDD+ has provided US$5.6 billion since 2008.

- JETPs promise a total package of US$46.5 billion for 4 countries.

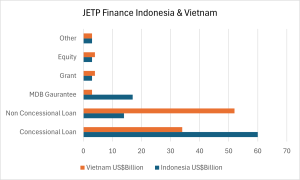

In Vietnam market-rates of interest on loans make up more than half the package. Even concessional loans, especially if disbursed through established multilateral development banks, may require sovereign guarantees from the government to assure lenders that the government will take certain remedial actions, should projects face challenges.

In other words, the JETP will inflate national and privately held debt position of the recipient countries. Whether loans are actually taken on is uncertain: internal vested interests and political economy factors will be hugely influential on what the energy sectors in these two countries actually does.

However, the point here is that health is in a dilemma:

Health systems need clean energy. Transitioning to clean energy generation and transmission is a necessary action to take.

But debt-based finance taken on by or guaranteed by the public sector has historically meant that health (and education and social services) will have to pay some of it back. A health sector pays back debt it didn’t take on by losing public investment, shrinking services, and pushing care into private sector provision.

The JETP has been described as innovative but the innovation offered is instrumental. Meaning goal-focused and operating within existing power structures so that winners continue to embed power while losers are ignored in favour of defining success in terms of function.

The New Collective Quantified Goal (NCQG) negotiated at COP29 promised $US1.3 trillion annually by 2035 to support LMICs respond to the climate crisis, consisting of at least $US300 billion annually through public finance from developed countries. However,

“the final agreement made no commitment to how much would come in the form of grants and highly concessional finance, which risks climate finance contributing to debt distress and means market-rate financing will continue to be counted the same as grant-based support. Furthermore, subgoals for mitigation and adaptation were not established, meaning no concrete progress to address the imbalance whereby only 6% of global climate finance goes towards adaptation” [13 emphasis added].

Conclusion

Pressures on government finances are a global phenomenon. Average debt-to-GDP ratios are rising and rising quickly in LMICs.

If a government borrows money from its own central bank and therefore holds a licence to print money to pay the interest and make repayments, this situation could be acceptable. But if debt is held externally in foreign currency, if interest rates are linked to inflation, if your country is suffering from relatively low economic growth (relatively lower than interest rates) then government finances are in trouble. And health sector has time and time again been part of the austerity measures to reduce such pressure on the public purse.

The green transition will expensive, but I don’t truly believe that debt is a sustainable answer. Living beyond our financial and ecological boundaries “needs to be confronted, (we need) to come back to living within our means” [14].

References

[1] UCSF Institute for Global Health Sciences & Open Consultants (2023) Improving Investments in Climate Change and Global Health: Barriers to and Opportunities for Synergistic Funding San Francisco: University of California

[2] Climate Policy Initiative https://www.climatepolicyinitiative.org/publication/top-down-climate-finance-needs/

[3] World Bank What You Need to Know About How CCDRs Estimate Climate Finance Needshttps://www.worldbank.org/en/news/feature/2023/03/13/what-you-need-to-know-about-how-ccdrs-estimate-climate-finance-needs

[4] Mckinsey & Co COP28: Climate Finance https://www.mckinsey.com/capabilities/sustainability/our-insights/sustainability-blog/cop28-climate-finance

[5] Independent High-Level Expert Group on Climate Finance (2022) Finance for Climate Action Scaling up Investment for Climate and Development

[6] World Bank Group (2023) International Debt Report 2023 Washington DC.

[7] Diamantis et al (2020) Government Debt Crisis and the Impact on National Health Systems: A Retrospective Study and Policy Recommendations to Greece. Cureus Http://www.doi:10.7759/cureus.10786.

[8] Brandao-Marques et al (2023) High Debt Levels can Hinder the Fight against Inflation https://cepr.org/voxeu/columns/high-debt-levels-can-hinder-fight-against-inflation

[9] World Bank (2023) Project Information Document https://documents1.worldbank.org/curated/en/099073003232326185/pdf/P1789570c5bfe0090af93002c7ee9a766f.pdf

[10] Coccia et al (2024) Negative Effects of High Public Debt on Health Systems facing Pandemic Crisis: Lessons from COVID-19 in Europe to Prepare for Future Emergencies AIMS Public Health https//www.doi:10.3934/publichealth.2024024

[11] Ordonez et al (2024) Just Energy Transition Partnerships and the Future of Coal Nature Climate Change https://doi.org/10.1038/s41558-024-02086-z

[12] Martinus M (2024) Just Energy Transition Partnerships (JETPs) in Indonesia and Vietnam: Implications for Southeast Asia ISingapore, ISEAS

[13] UN Trade and Development (2024) Countries agree $300 billion by 2035 for New Climate Finance Goal – What Next? https://unctad.org/news/countries-agree-300-billion-2035-new-climate-finance-goal-what-next

[14] House of Lords Economic Affairs Committee (2024) 1st Report of Session 2024–25 HL Paper 5 National Debt: It’s Time for Tough Decisions London, House of Lords