This post was revised and edited on 1st July 2025.

Impact investing is “investments made with the intention to generate positive, measurable, social or environmental impact alongside a financial return” [1]. Intentional is important – it means impact doesn’t happen by accident.

Impact investing was valued at US$1.571 trillion in 2023, managed by 3,907 organisations [2].

The question of impact is not new to global health. Universal Healthcare Coverage, for instance, is an impact investment made by governments, bilateral donors, multilateral development banks, international organisations, foundations and charities, religions and political organisations, as well as individuals.

However, the term ‘impact investing’ is increasingly associated with private finance. As is the case with private finance generally, impact investing is diverse, complex, and can lack transparency.

But who are these impact investors? Are they all private? Do they behave differently to other private profit-seeking investors? And can impact investing genuinely work for, rather than extract from, climate resilient biodiversity positive healthcare in low resource settings?

State of the Market

First, for clarification, impact investing is different from finance called ESG (Environmental, Social, Governance). ESG is a much larger investment market though the size of the ESG market depends on the definition of ESG in use. Over the last few years, there has been a welcome tightening on rules around ESG claims to tackle greenwashing. ESG finance is considered to be risk-averse finance [3].

The Global Network on Impact Investing published a state of the market in 2024. I’ll summarize a few key points focusing on the identity of investors:

- Investment fund managers were the most numerous type of investor but pension funds had the greatest volume of impact funds under management (also called Assets Under Management or AUM);

- The third most common type of organization was insurance companies and banks and, together, these two controlled 37% of global impact investment money;

- Development finance institutions were somewhat more numerous than banks, insurance companies, and foundations. Notably, there were less foundations active in impact investing but these were managing a similar volume of funds as the development finance institutions;

- Sovereign wealth funds (savings held by government), family offices, and endowments were the smallest types of investors and managed the smallest share of impact assets-under-management globally.

The vast majority of investors reside in US, Canada, and Europe.

The regions of East & Southeast Asia accounted for 7% of global impact funds and 6% of global impact investors. The share of impact investors compared to funds under management was higher in Southeast Asia (and on par with Oceania) suggesting more investors have smaller pots of money to invest compared to East Asia. In Southeast Asia, these investors appear to be wealthy families investing directly as philanthropy rather than market-rate seeking institutional investors [4].

So, in 2023, if you had wanted to maximize access to impact funders you would have targeted pension providers, investment fund managers, insurance companies and banks. And you would have been talking to investors in the Global North.

Crowdfunding isn’t mentioned in the report, but it is an important platform for accessing and pooling impact funds.

Pension funds appear to be a significant impact investor. With increased participation of these institutional investors (rather than individuals, individual families, or government, or the development finance institutions) the majority (74%) of impact investors want a market-rate-of-return otherwise known as a risk-adjusted-return [1]. The remainder accept below-market-rate-of-return or very-low-return (close to return of capital). The number of impact investors willing to accept these lower and low returns is falling [5].

Institutional investors are also looking for large investment opportunities. For new areas of investment like nature-based-solutions, the capital required by an investee (project) can be relatively small but that smallness can be a barrier to entry for institutional investors “ who need to minimise their transaction costs”. For these large institutional investors, “it is easier to raise US$400 million than US$4 million” [6].

Like other types of finance, impact investing is shaped by local and international politics, local power dynamics, and policy and legislation frameworks. The history of renewable energy development, for instance, shows that investment isn’t only shaped by rates-of-return. Rather investment decisions are influenced by policy trade-offs, potential and achievable technological outcomes, context-specific political priorities, government-private sector relations, national and multi-level governance structures in a region, market structures, as well as stakeholder vested interests [7].

Who is Investing in Climate, Biodiversity, and Health for Impact?

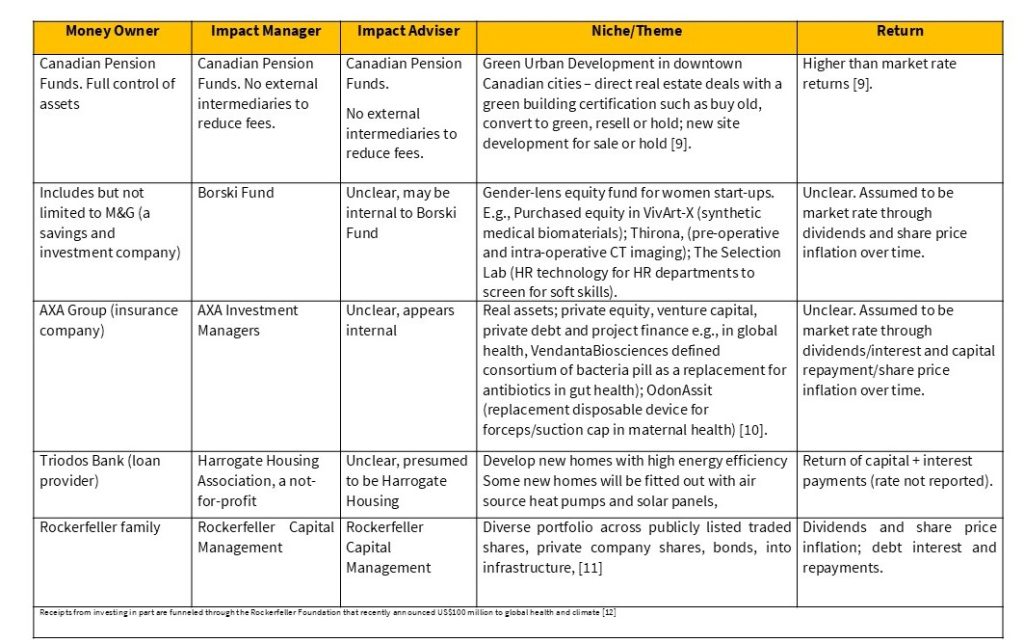

The GIIIN analysis gives an overview of categories of investors but to get a sense of who these are in reality, let’s take a quick look at activities reported by the Impact Investor magazine [8] with a few exceptions (referenced in individually).

It’s interesting to see just how diverse and collaborative impact investors are. The GIIN typology discussed earlier is useful, though clearly simplifies complexity. Impact investors, it seems, hate working alone.

Press reports in the Impact Investor magazine can be low on detail (e.g., on returns, measures of genuine impact) but they do highlight the level of activity and optimism around impact investing.

So how does it work in reality?

Follow the Money

Following the Money is a useful way to find out how money moves, who the critical stakeholders are, and who is receiving greatest benefit.

Let’s use green buildings because this sector is relatively mature, has accepted green certifications, is a critical area for decarbonization of healthcare, and is the inspiration for this blog.

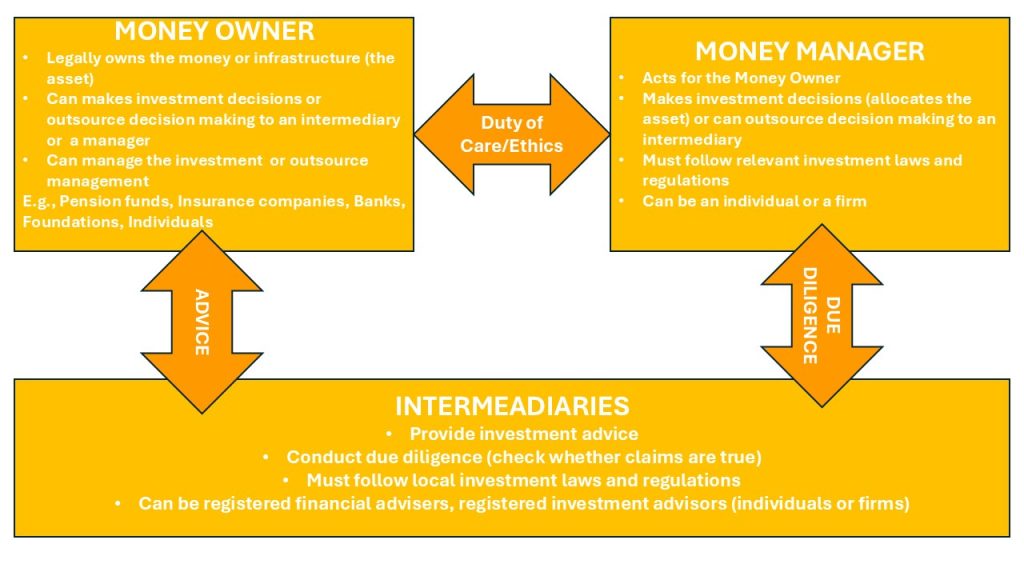

Let’s imagine you, dear reader, are an impact investor. That makes you the asset owner in the jargon of the financial industry. In this example, though, I’m going to call you the money-owner for clarity.

There could be three stakeholders involved in finding and managing an impact investment. The money owner, the money manager, and an advisor-intermediary. These could be one and the same stakeholder (e.g. as in pension funds) or split.

You, the money owner, have a significant amount of money to invest in a green activity.

The first thing to do is decide on where to allocate your money. You aren’t sure so you ask advice from an intermediary called an investment advisor. She advises putting all your money into a green building option called Living Building Challenge (LBC) building because LBC is the highest green building standard available and externally verified on performance. By doing so, you’ve tried to tackle the problem of greenwashing from the beginning.

You’d rather not manage this investment yourself, so you find a money-manager (in finance industry jargon, asset manager) to do it for you.

Based on my understanding of how the money flows, as the money-owner, your simplified investment process could look like this:

I have seen this called an investment cycle. But from your point of view as the money-owner, it looks linear because you want in; you want a return on your investment; and at some point you want out (exit).

As an exemplary impact investor, you generate impact across this process by:

- Deciding what to invest in – an evidenced solution to a climate pollution problem and in which climate & biodiversity gain is embedded into the model. You eliminate greenwashing by conducting checks on the claims made by the investee (called ‘due diligence’ in the finance industry);

- After handing over your money, you continue to actively engage with your money manager throughout, ensuring that impact stays on track. As part of this, a responsible exit plan is created that prioritises long term environmental goals with perhaps a set of key performance indicators whose achievement flags to you when it is time to exit [3];

- At point of exit, you prioritise long-term social or environmental goals (not short-term financial gains by selling when share prices are estimated to be at their peak). So you patiently follow your impact exit plan. You don’t expect your exit to be quick. You actively seek other values-aligned impact investors who are additionally investors that can further grow the business of the investee. You also facilitate an extended getting-to-know-you period between the investee and the new investor to ensure a smooth transition [13].

All of this sounds familiar with best practice for donor transition in global health development [14] and seems to imply greater engagement with investments on the part of an impact investor when compared to a commercial investor.

More Questions Less Answers

There are sectors and communities that can’t be served by private finance. The narrative of private finance, and private impact investing is that the private sector is critical to decarbonization and biodiversity regrowth. However, there are niches that don’t fit with market-return impact investing. AXA, a multinational insurance corporation, call these ‘no-go-zones’ [10].

But I still more questions than answers.

For whom does impact accrue? If there are at three stakeholders involved in a deal, can all of these genuinely claim climate and biodiversity impact? There seems to be scope for double counting of impact and over-estimating each stakeholder’s contribution to genuine change.

When does impact accrue? If the original money-owner, invested in a company providing solutions to pollution and biodiversity loss, and then sells their shares to a new money-owner, does this second and subsequent transactions (called secondary market) create impact? There would be no new capital for the investee because the sale of shares would benefit the original money-owner only. At the same time, there would still be a need for the investee to generate return for the new money-owner but these transactions don’t seem to provide an investee with additional working capital. From the point of view of impact, is the new money-owner creating new impact or riding on historically created impact?

Wouldn’t this further imply that impact key performance indicators (KPIs) have to change as investees and their projects mature?

So does attribution of impact matter? And how do we deal with attribution to avoid greenwashing?

What rates-of-return are impact investors actually getting? The Canadian Pension Funds, for instance, invests in green buildings and this brings benefits to property developers and the construction industry, as well as providing new property for purchase, rent, and use to individuals and pension returns for its investors. It sounds like everyone is winning – but are rates of return for one stakeholder obtained at the expense of another?

And so…

I realise in writing this post that I had been conflating the ultimate money-owner (the asset owner), the money-manager, and the investee, and this made it harder to understand how the money actually moves. Separating out these roles and understanding the different perspectives involved helps to identify where the potential financial and impact returns can be obtained by different stakeholders.

Ultimately, like other private finance, the impact investor is footloose. An exit will be sought at some point, even if that exit could take longer than a commercial financial deal and be conducted in a values-aligned way.

Finally, is it moral to translate every human action into a business deal? The language of a common good is missing:

“The Global North has this tendency of going in and investing in companies and ignoring the rest of the system. If you want to create lasting impact, it’s about transforming all the local entities that are around these vulnerable communities” [15].

References

[1] Global Impact Investing Network https://thegiin.org/publication/post/about-impact-investing/#what-is-impact-investing

[2] Hand et al (2024) Sizing the Impact Investing Market 2024 The Global Impact Investing Network, New York

[3] Clark et al (2023) Impact Due Diligence and Management For Asset Allocators: A Field Guide Bluemark

[4] Ben Thornley interview by The Asset https://www.theasset.com/article-esg/53605/rise-of-asia-impact-investing-challenges-trends-and-innovations

[5] Vega et al (2025) A Multistakeholder Approach To Impact Investing: Focus On Institutional Investors And Key Dimensions Research in International Business and Finance https://doi.org/10.1016/j.ribaf.2025.102766

[6] Baralon et al (2022) Common Success Factors for Bankable Nature-based Solutions World Wildlife Fund & South Pole

[7] Ragosa et al (2024) The Political Economy Of Electricity System Resource Adequacy And Renewable Energy Integration: A Comparative Study Of Britain, Italy And California Energy Research & Social Science https://doi.org/10.1016/j.erss.2023.103335

[8] Impact Investor www.impact-investor.com

[9] Beath et al (2022). Green Urban Development: The Impact Investment Strategy of Canadian Pension Funds Journal of Sustainable Real Estate https://doi.org/10.1080/19498276.2022.2125203

[10] AXA Investment Managers Investing for People and Planet Impact Investing – Private Markets 2023 Annual Review AXA Group

[11] The Rockerfeller Family Office (2024) The Rockerfeller Investing Guide

[12] Rockerfeller Foundation https://www.rockefellerfoundation.org/news/the-rockefeller-foundation-commits-usd-100-million-to-test-and-scale-climate-and-health-solutions-globally/

[13] Gilbert (2018) How To Invest -and Exit – With Impact and Return https://bthechange.com/how-to-invest-and-exit-with-impact-and-return-9639e0d9d98f

[14] Gilbert et al (2019) Sustainable Transition from Donor Grant Financing – What Could it Look Like Asia Pacific Journal of Public Health www.doi.org/10.1177/1010539519870656

[15] Agustín Vitórica, GAWA Capital COFIDES Launches €200m Climate Mitigation and Adaptation Fund www.impact-investor.com